Key Points

• Indigenous crude contributes only a small share to overall consumption

• Transport fuels dominate demand, driving external dependence

ISLAMABAD: Pakistan’s petroleum sector presents a structural paradox: the country refines a significant portion of its fuel domestically, yet remains heavily dependent on imports due to limited indigenous crude oil production.

According to the Ministry of Energy, Pakistan’s oil refining sector includes five major, mostly aged refineries with a combined, often underutilised capacity of ~450,000 b/d (~20 million tons/year), struggling with low-tech hydroskimming technology.

In supplying the essential fuel, they produce a high level of furnace oil and rely heavily on crude imports, prompting a government drive towards upgrades and Euro-5 standards.

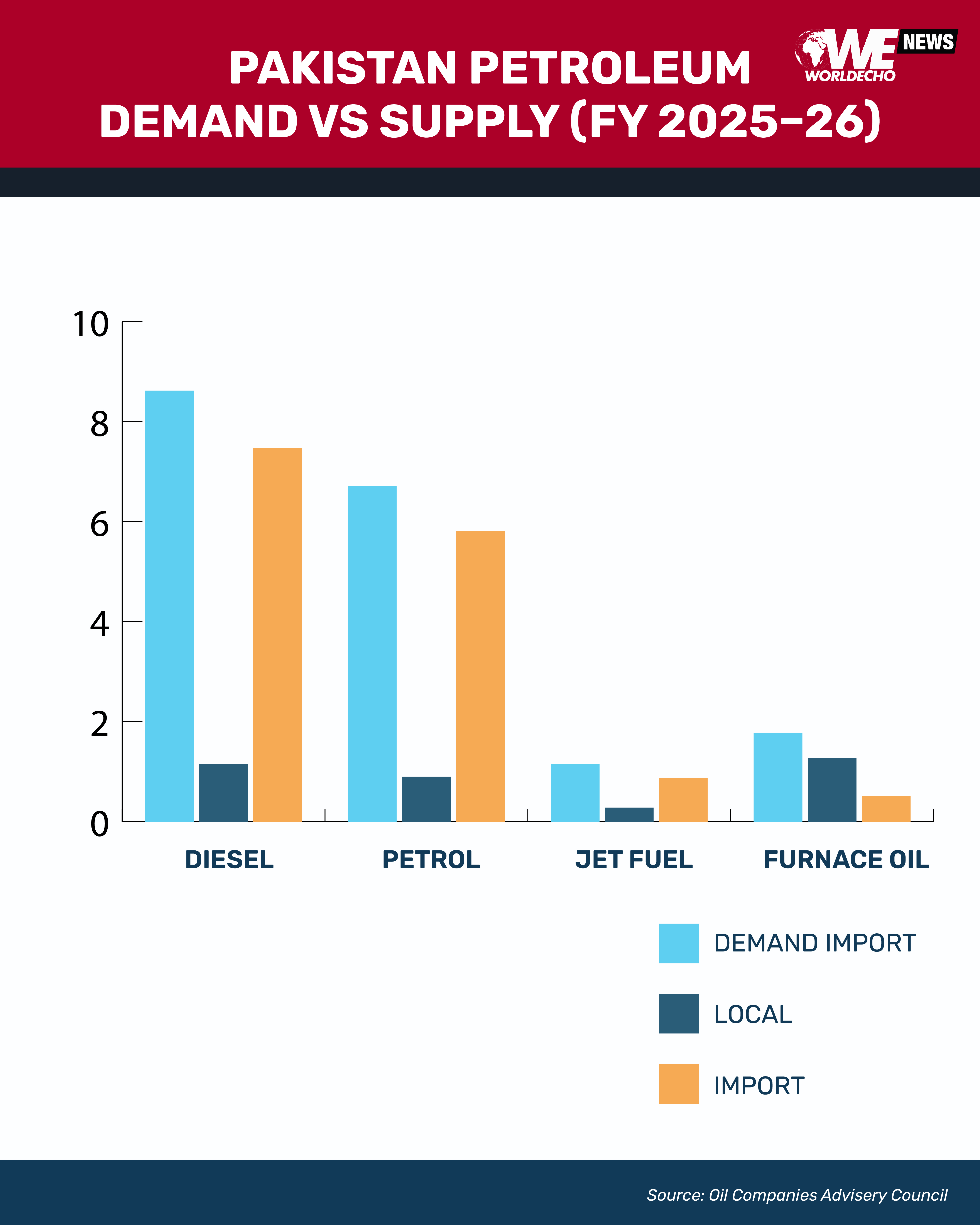

Demand profile led by transport fuels

Data compiled by the Oil Companies Advisory Council (OCAC) for fiscal year 2025–26 show that Pakistan consumes roughly 18-19 million metric tonnes (MMT) of petroleum products annually.

Diesel leads demand at 8.62 MMT, followed by petrol at 6.71 MMT, jet fuel at 1.15 MMT, and furnace oil at around 1.78 MMT.

For global readers, petroleum volumes are reported in metric tonnes (tonnes), a mass-based unit preferred in the oil industry because fuels expand and contract with temperature, making volume measures less reliable across markets.

One metric tonne equals 1,000 kilograms, and MMT refers to one million metric tonnes. This standard enables consistent comparison of crude and refined products across countries despite differences in density and temperature conditions.

In Pakistan’s case, the dominance of diesel and petrol reflects a transport-heavy economy where road freight and passenger mobility drive energy use.

Refining capacity versus real production

At first glance, Pakistan appears to have a relatively developed downstream petroleum sector. Around 55 to 60 per cent of its fuel demand is met through local refining, meaning crude oil is processed within the country into usable products such as petrol, diesel and byproducts.

However, this figure can be misleading. Refining is only one part of the energy supply chain. The critical constraint lies upstream, in crude oil production.

Pakistan produces only about 3 to 4 MMT of crude oil annually. This limited output means that most of the crude processed in local refineries is imported. In practical terms, the country is refining fuel domestically, but using foreign raw material.

This distinction is important in economic terms. Fuel derived from imported crude is still counted as an import in the balance of payments calculations, even if it is processed locally.

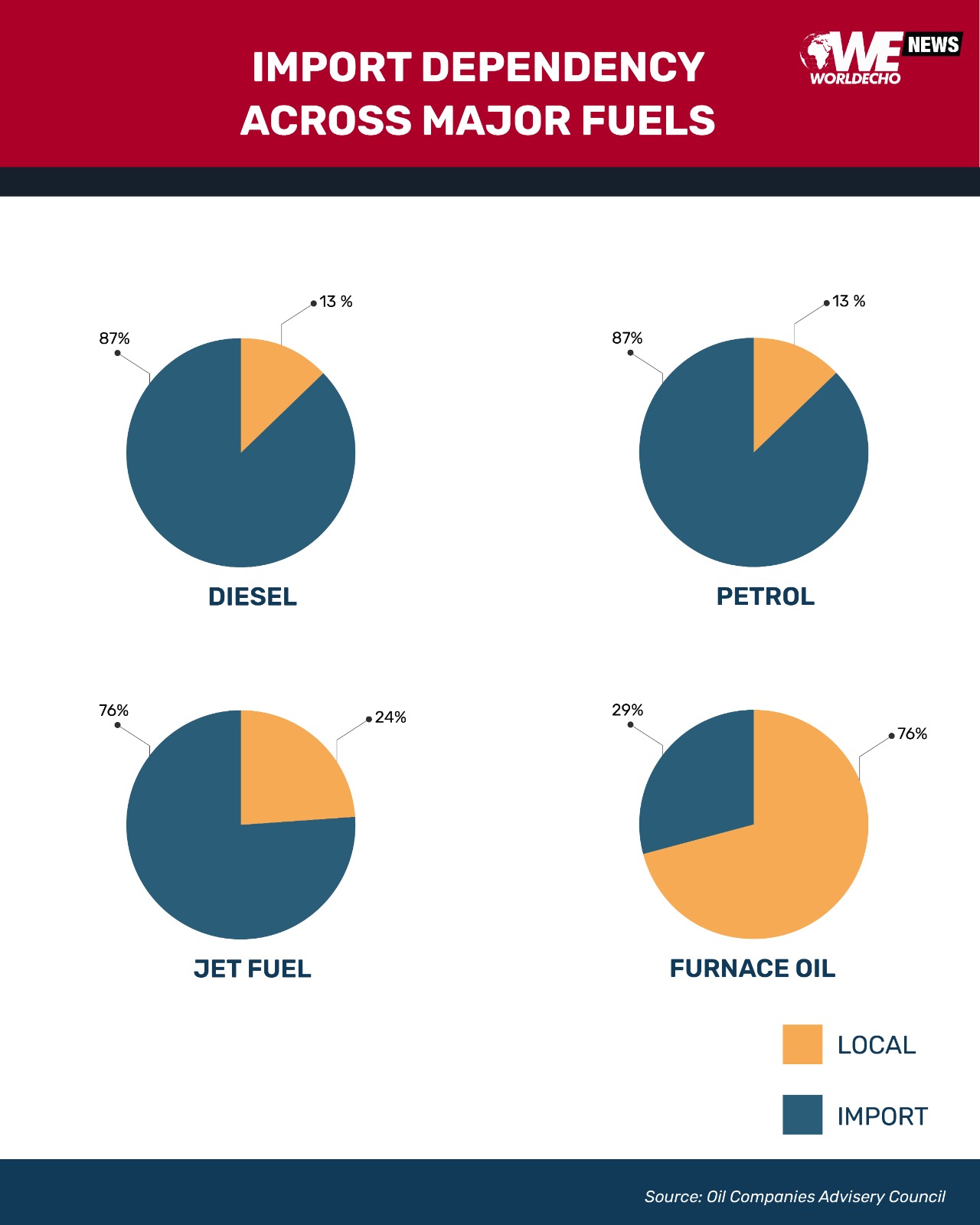

Breaking down import dependence

A closer examination of individual fuels highlights the extent of this reliance.

Diesel, the backbone of Pakistan’s transport and agricultural sectors, has a total demand of 8.62 MMT.

Of this, only about 1.15 MMT—roughly 13 per cent—comes from indigenous crude. The remaining 87 per cent is linked to imports, either as refined diesel or crude oil later processed domestically.

Petrol shows a similar pattern. Out of 6.71 MMT in demand, just 0.90 MMT, or about 13 per cent, is locally sourced in true terms. The bulk is again dependent on imports.

Jet fuel, used in aviation, has a somewhat higher local contribution at around 24 per cent, though imports still account for more than three-quarters of supply.

Furnace oil presents a partial exception. About 71 per cent of its supply is linked to local refining output, largely due to the way refineries process crude into different products, known as the yield structure.

Even so, part of this output is still based on imported crude.

The misconception around “local” fuel

Energy analysts often stress the need to distinguish between “local refining” and “indigenous production.”

In public discourse, these terms are sometimes used interchangeably, creating a perception that Pakistan is more self-sufficient than it actually is.

In reality, true indigenous contribution—fuel produced from domestically extracted crude—remains limited.

Estimates suggest that only about 10 to 15 per cent of petrol and diesel consumption originates from local resources, with slightly higher shares for jet fuel and furnace oil.

This gap between perception and reality has implications for policymaking and public understanding, particularly when assessing energy security.

Implications for the external account

Pakistan’s reliance on imported petroleum products and crude oil has direct consequences for its external account, a key economic indicator that tracks a country’s foreign currency inflows and outflows.

Fuel imports constitute a significant portion of the national import bill.

When global oil prices rise, Pakistan’s energy import expenditure increases, putting pressure on foreign exchange reserves and the national currency.

Conversely, any global supply chain disruption can create risks for domestic fuel availability, underscoring the strategic importance of energy security.

Policy responses and structural challenges

Successive governments have attempted to reduce this dependence through a combination of strategies.

These include promoting oil and gas exploration to boost domestic production, upgrading refinery configurations to improve efficiency, and diversifying the energy mix towards alternatives such as renewables and natural gas.

There have also been efforts to manage demand through pricing reforms and energy conservation measures, though these often face political and social constraints.

Despite these initiatives, progress remains gradual. Structural factors—such as limited geological discoveries, rising demand, and infrastructure constraints—continue to shape the sector’s trajectory.

A system exposed to global shifts

For global observers, Pakistan’s petroleum landscape illustrates a broader challenge faced by many emerging economies: balancing domestic capacity with external dependence.

The country’s refining base provides a degree of operational flexibility, allowing it to process crude locally and manage supply chains more effectively.

Yet the underlying reliance on imported raw material leaves it exposed to international price fluctuations and geopolitical developments in oil-producing regions.

The result is a hybrid system—partly local in operation, but globally dependent in substance—where energy security remains closely tied to external dynamics.