Key Points

- Government begins scenario analysis of global economic fallout from Iran war

- Authorities move to strengthen capital markets and ensure financial stability

- Export sectors urged to maintain competitiveness amid global uncertainty

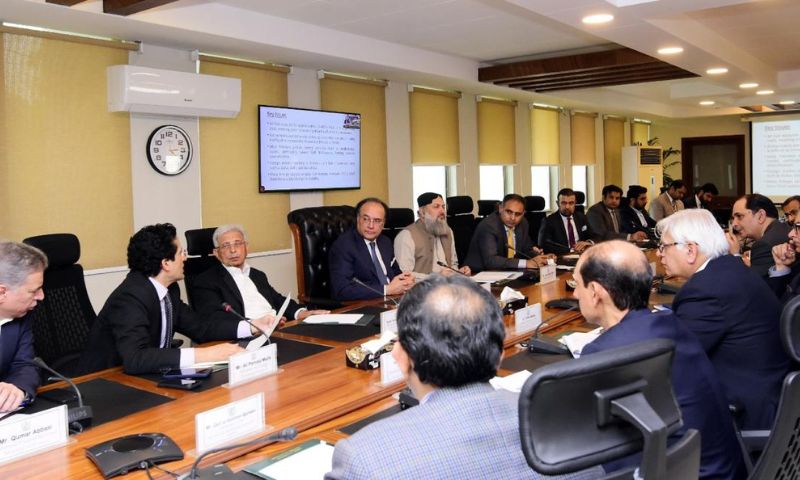

ISLAMABAD: Pakistan’s finance minister on Wednesday held a series of separate consultations with financial regulators, banks and export industry leaders as stepped up monitoring of potential economic risks arising from the expanding Iran war.

Analysts and observers warned that the conflict could spill into global financial and energy markets after an attack on a financial institution in Iran.

The engagements came hours after reports that Iran warned of targeting economic interests after an attack on one of its banks.

The latest warning has heightened concerns that the conflict could increasingly move into financial and economic domains.

Finance Minister Senator Muhammad Aurangzeb chaired a meeting of the Capital Market Development Council (CMDC), held a virtual consultation with the Pakistan Banks’ Association (PBA), and separately met leaders of export-oriented industries to assess the evolving situation and reinforce economic resilience.

Capital market reforms

Speaking at the CMDC meeting, Aurangzeb stressed that strengthening Pakistan’s capital markets remained critical for ensuring sustainable economic growth.

Financial stability, particularly during periods of heightened global uncertainty, is the top priority of the government, he added.

He said a strong and well-functioning capital market would enable corporations to access long-term financing.

A sustainable market also reduces excessive reliance on bank lending, allowing the financial system to become more balanced and resilient, he added.

The minister underscored the need to accelerate reforms aimed at deepening Pakistan’s corporate bond market.

He described it as an important mechanism for mobilising domestic savings and supporting private-sector investment.

He directed regulators and market institutions to address bottlenecks across the capital market ecosystem.

The bottlenecks include issuance procedures, regulatory approvals, market infrastructure and liquidity in secondary markets.

Aurangzeb also asked the Securities and Exchange Commission of Pakistan to intensify outreach to corporates and investors.

The Minister required the corporate regulator to ensure that stakeholders were fully aware of recently introduced regulatory reforms designed to simplify corporate bond issuance and improve market access.

Banking sector coordination

In a separate virtual meeting with the Pakistan Banks’ Association led by Chairman Zafar Masud, the finance minister discussed the evolving regional situation and the importance of maintaining financial stability and uninterrupted banking services.

Aurangzeb told banking leaders that the government had established a high-level coordination mechanism involving key economic ministries and institutions to monitor developments in global markets and assess potential implications for Pakistan’s economy.

The government, he said, was conducting regular scenario analysis to evaluate possible impacts on inflation, external accounts and broader macroeconomic stability.

Authorities are also closely tracking developments in global supply chains and energy markets.

The rising tensions in the Gulf have already increased volatility and raised concerns over potential disruptions to oil shipments through the Strait of Hormuz.

The minister emphasised that ensuring continuity of essential supplies and maintaining macroeconomic stability remained the government’s immediate priority.

Zafar Masud briefed the minister on preparedness measures undertaken by the banking sector, including coordination frameworks designed to facilitate information sharing and ensure uninterrupted financial services.

Engagement with export industry

Aurangzeb also met representatives of leading export-oriented industries, including textile and apparel manufacturers, in consultations led by Pakistan Regional Economic Forum Chairman Haroon Sharif.

During the meeting, the minister reaffirmed that strengthening export competitiveness remained central to Pakistan’s economic revival strategy, particularly as global economic uncertainty increases.

He emphasised the importance of improving productivity, encouraging technological innovation and moving into higher-value market segments to strengthen Pakistan’s position in international supply chains.

Industry leaders stressed the need for a supportive tax and regulatory environment that encourages reinvestment and expansion, particularly in value-added textile segments that account for a major share of Pakistan’s export earnings.

Participants also highlighted the importance of modernisation, digital transformation and technology adoption in maintaining competitiveness in global markets.

Business leaders urged the government to review cost structures and regulatory levies affecting export-oriented industries in order to sustain growth and employment in the sector.