Key Points

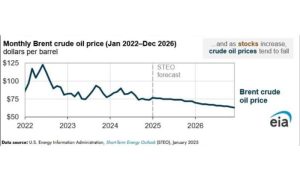

- Brent crude trades around $60–61 per barrel and WTI near $57 amid ample global supply

- Venezuela holds about 303 billion barrels of oil, mostly heavy crude, but produces under 1 per cent of global output

- Any easing of US sanctions could gradually add hundreds of thousands of barrels a day to supply

- US Gulf Coast heavy-oil refineries stand to benefit most from a potential Venezuelan return

- Investors are pricing timelines and refinery economics, not political drama

ISLAMABAD: Global oil markets have absorbed the latest US action against Venezuela with notable restraint, keeping prices anchored near multi-year lows despite geopolitical escalation and American refiners are already eyeing Venezuelan heavy oil.

Brent crude was trading around $60–61 a barrel this week, with US West Texas Intermediate near $57, reflecting investor confidence that immediate supply risks remain limited in an already well-supplied market. The United States’ latest action against Venezuela has reopened one of the most consequential questions in global energy markets: what happens if the world’s largest oil reserve holder is gradually re-integrated into global supply chains after years of sanctions and collapse.

The marked reaction

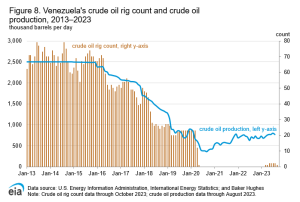

The calm, traders say, stems from numbers rather than narratives. Venezuela today produces roughly 800,000 to 900,000 barrels per day, which accounts for less than 1 per cent of the global output of almost 102 million barrels per day. That scale is too small to shock prices in the short term. That response reflects a deeper reality. This episode is not being priced as a geopolitical shock. It is being assessed as a structural energy story, centered on heavy crude, refinery economics, sanctions architecture and long-term supply balance.

Yet beneath the surface, investors are closely evaluating what could follow if the sanctions policy shifts and Venezuelan oil is gradually reintegrated into the global market.

Why Venezuela still matters

Venezuela matters not because of what it pumps today, but because of what it holds. With proven reserves estimated at about 303 billion barrels, the largest in the world, the country represents the biggest untapped oil option embedded in the global energy system. Two decades ago, Venezuela pumped more than 3 million barrels per day. By 2024–25, output had collapsed to roughly 800,000–900,000 barrels per day due to underinvestment, loss of technical capacity, sanctions, and infrastructure decay. The country shifted from being a major global supplier to a marginal exporter.

Years of sanctions, mismanagement and capital flight did not erase those reserves. They dismantled the infrastructure needed to convert them into exportable barrels. Yet dismissing Venezuela as irrelevant misses the core issue.

Story of Venezuelan heavy crude

The defining feature of Venezuelan oil is quality. Most of it is heavy or extra-heavy crude, capital-intensive to extract, technically complex to process and dependent on specialised upgrading and refining capacity. This makes Venezuela structurally different from light shale producers and central to a specific segment of the oil market.

The US oil refinery structure

That segment, refining the heavy oil, is concentrated in the United States. Over the decades, US refiners, particularly along the Texas and Louisiana Gulf Coast, invested heavily in complex facilities designed to process heavy crude. The United States now hosts six of the world’s largest heavy-oil refineries. Heavy crude imports, which accounted for roughly 15 per cent of US refinery feedstock in the 1980s, have risen to close to 70 per cent today.

Sanctions on Venezuela have forced these refineries to rely more heavily on Canadian heavy crude and alternative grades, often at a higher cost and with increased logistical complexity. From an investor perspective, the fit between Venezuelan heavy oil and US refining capacity is structural rather than coincidental.

Sanctions and Venezuelan oil exports

Whether that fit translates into renewed trade depends on sanctions. US officials have signalled that oil sanctions would initially remain in place even under a new political arrangement, using energy exports as leverage. At the same time, Washington has openly discussed the potential return of US oil majors, infrastructure rehabilitation and a redirection of Venezuelan crude toward US and allied markets if conditions are met.

Will a new regime allowed to export oil?

The central market question is not regime change itself, but sanctions policy. U.S. officials have indicated that oil sanctions would remain initially, even under a new leadership structure, and would be used as leverage. That suggests no immediate surge of Venezuelan barrels.

However, policy signals also point to conditional relief. U.S. leaders have openly discussed the return of American oil majors, reconstruction of oil infrastructure, and redirection of Venezuelan crude toward U.S. and allied markets.

Analysts at Goldman Sachs and cited by Reuters estimate that with sanctions relief and investment, Venezuela could raise output to about 1.3–1.4 million barrels per day within one to two years. A return toward 2 million barrels per day would take longer and require sustained capital inflows. This timeline is critical. Markets are not pricing today’s barrels. They are pricing the probability distribution of future supply.

Analysts estimate that with sanctions relief and sustained investment, Venezuela could increase production to about 1.3 to 1.4 million barrels per day within one to two years. A return toward 2 million barrels per day would take longer and require billions of dollars in capital, technical rebuilding and regulatory clarity. Investors are not pricing an immediate surge. They are pricing probabilities over time.

Global supply and demand dynamics

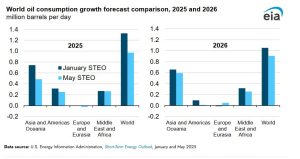

The broader supply backdrop explains the muted reaction. The International Energy Agency expects global supply to exceed demand growth into 2026, keeping pressure on prices. OPEC+ has adopted a cautious output strategy, which could offset the risk of oversupply and geopolitical uncertainty. In this environment, incremental Venezuelan barrels would likely weigh on prices rather than lift them, particularly in heavy crude differentials rather than headline benchmarks.

Who wins and who loses

The winners and losers are already visible. US Gulf Coast refiners configured for heavy crude would benefit from improved access and margins on the feedstock. US energy companies with legacy Venezuelan expertise could see long-term profit opportunities. Competing heavy crude suppliers could face tighter pricing, and producers in an already crowded market would confront additional competition.

Weather and Timing

Seasonal and weather factors remain an overlay rather than a driver. Winter distillate demand, hurricane risks in the Gulf of Mexico and summer driving patterns will continue to shape short-term price movements. Any Venezuelan supply return during periods of weak seasonal demand would amplify downward pressure, whereas stronger demand or supply disruptions elsewhere would soften its impact.

Bottom line

US actions against Venezuela have not shaken oil markets because the immediate supply impact remained limited. The long-term implications, however, are significant.

If the sanctions ease and US majors re-enter the market, Venezuela could gradually re-emerge as a meaningful supplier of heavy oil. That would reshape refinery economics, after heavy crude pricing and the addition of supply to an already competitive global market. For now, investors are doing what they always do best: separating signal from noise. The absence of a price spike does not reflect indifference. It reflects assessment. Venezuela’s oil potential is vast, but slow-moving. Infrastructure must be rebuilt, capital must return, and sanctions must unwind in stages.

Investors are not trading politics. They are trading timelines, refinery configurations and supply elasticity.