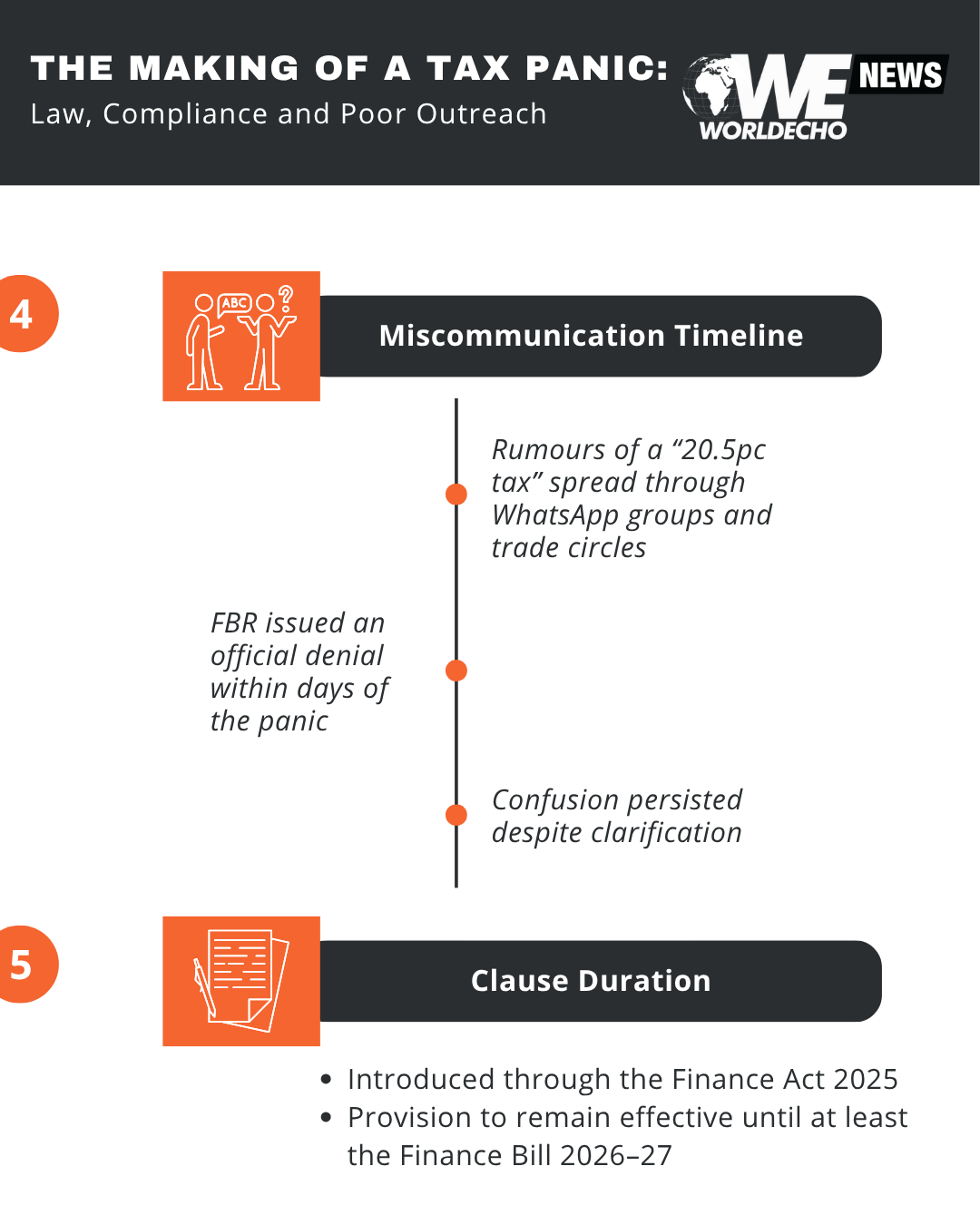

ISLAMABAD: When rumours of a 20.5 per cent tax on cash transactions above Rs 200,000 started making the rounds on social media and trade circles last month, they sparked swift and widespread anxiety.

Markets buzzed with speculation, small traders grew anxious, and even some seasoned tax consultants struggled to explain the alleged levy. Within days, the Federal Board of Revenue was compelled to issue a rare and pointed denial: no such tax exists.

Still, the reality is more layered—and far more consequential.

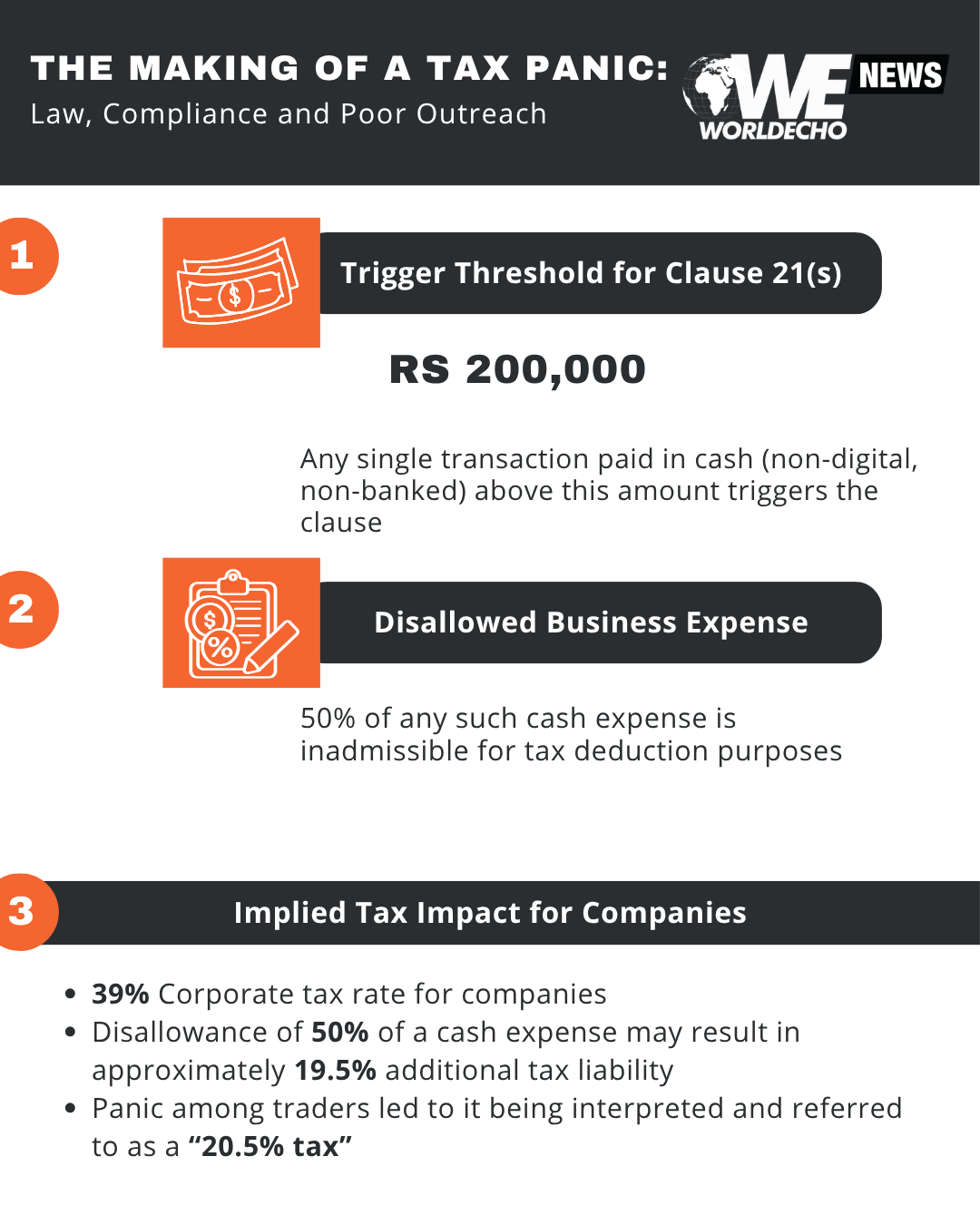

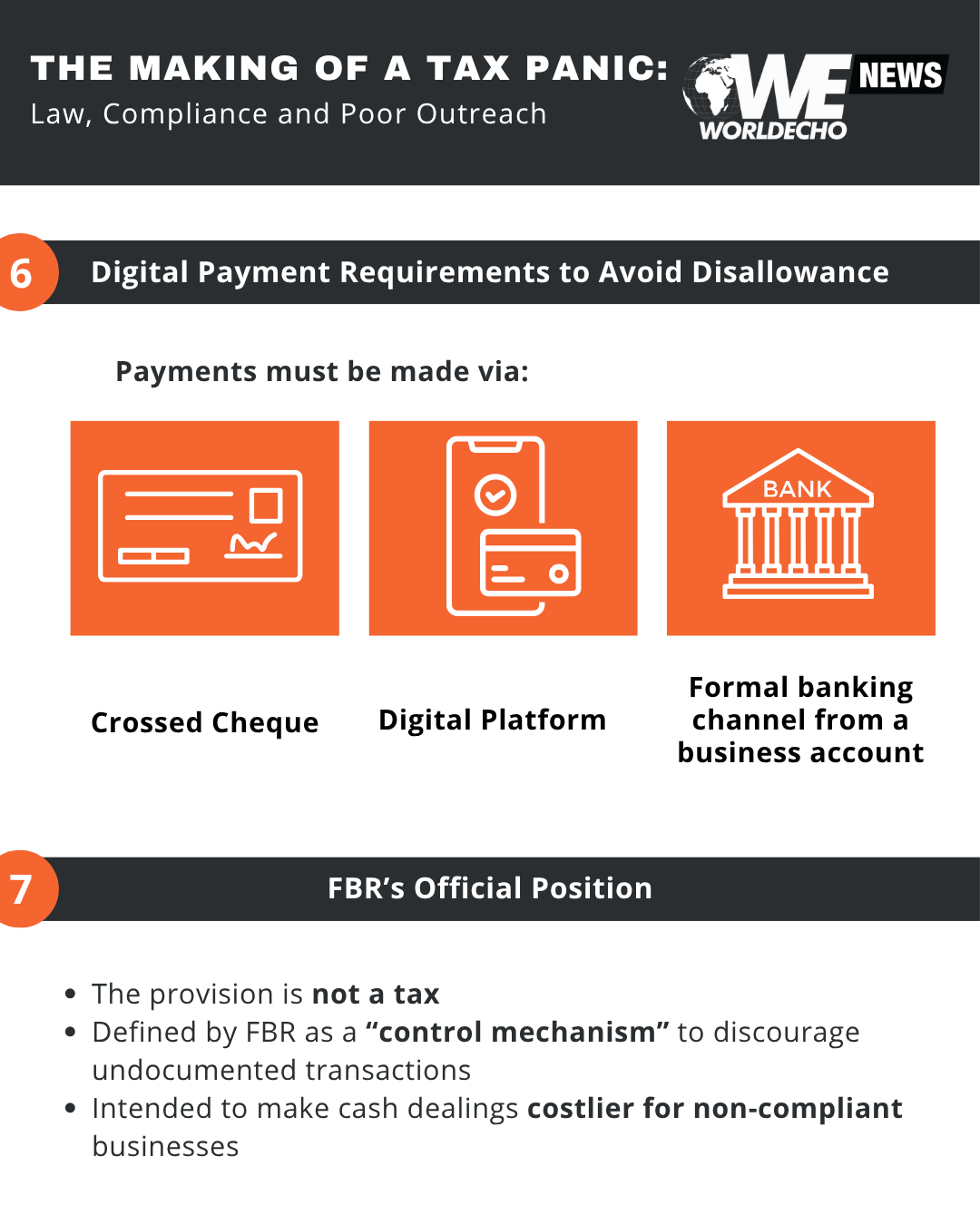

At the heart of the controversy is the clause ‘S’ of Section 21 of the Income Tax Ordinance, inserted through the Finance Act 2025. Though it introduces no new tax rate, it brings in a measure that, in practice, feels like a wolf in sheep’s cloting to those reliant on cash: the disallowance of 50 per cent of business expenses paid in cash above a Rs 200,000 threshold. It is not a revenue measure, officials insist, but a control mechanism.

Section 21, Clause (s) – “Where any expenditure in a single transaction exceeds Rs 200,000 and is made otherwise than by a crossed cheque drawn on a bank or through digital means from a business account, fifty per cent of such expenditure shall be inadmissible.”

“The idea is to tighten the noose around undocumented transactions,” says a senior FBR policy official, speaking on condition of anonymity. “This isn’t about taxing the cash itself —it’s about making cash transactions costlier to businesses that prefer opacity.”

Misread or miscommunicated

The provision reads plainly: if a business pays over Rs 200,000 for a purchase and does not use a crossed cheque, digital platform, or formal banking channel, half of that expense will be inadmissible for tax purposes. In effect, the remaining 50 per cent will not reduce the taxpayer’s declared income, leading to a bigger bite from taxable profits—and yes, a higher tax bill.

For a taxpayer in the highest tax bracket (39 per cent for companies), the disallowed 50 per cent could translate into an effective additional tax of nearly 20 per cent—hence the origin of the “20.5 per cent tax” claim. But that is an interpretation, not carved in stone.

The FBR’s clarification was emphatic but perhaps too late, as much of the business community had already internalised the measure as a direct penalty on cash dealings. “This is a failure of policy communication,” says tax analyst Faheem Yousuf. “You can’t bury a behavioural change like this in legal jargon and expect traders in Gujranwala or Larkana to get it from a Gazette notification.”

Reform without infrastructure

The policy reflects a growing shift in Pakistan’s tax architecture: a preference for deterrents over enforcement. Instead of catching tax evaders through audits and raids, the state is now going through the back door—quietly penalising non-documented behaviour through the back door—by disallowing expenses, capping deductions, or shrinking eligibility for refunds.

FBR Chairman Rashid Mahmood Langrial, in his briefing to the Senate Standing Committee on Finance, acknowledged that the law was passed after committee deliberations and will not be reversed before the next finance cycle. “This provision is here to stay until at least the Finance Bill 2026–27,” he said. “The intent is not revenue but documentation. If we don’t move towards formalisation now, we’ll keep bleeding on both the fiscal and governance fronts.”

But critics argue that such formalisation cannot stand on its own two feet.

“Most retailers and wholesalers still do not have access to reliable digital payment systems,” says Naeem Mir, a leader of the All Pakistan Anjuman-e-Tajiran—a traders’ representative body.

“If you penalise cash without enabling alternatives, you’re not encouraging compliance—you’re squeezing the vulnerable.”

Between policy & practice

The dilemma is not unique to Pakistan. Across the developing world, tax authorities face the impossible task of extracting more from shrinking formal sectors while trying to widen the tax base net. But Pakistan’s approach—particularly since the International Monetary Fund (IMF)-backed fiscal restructuring began—has increasingly leaned on incentivised digitisation.

Purchases made outside formal banking channels are already being flagged by tax profiling systems. Banks are now required to report large cash withdrawals, while retailers exceeding certain thresholds are mandated to integrate point-of-sale (POS) systems. The new clause introduces yet another behavioural nudge—this time through the spectre of a that hits where it hurts—but without the support systems that such nudges typically require.

Uncertainty for businesses

While FBR has denied the existence of a “20.5 per cent tax,” it has yet to issue a comprehensive user-friendly guide or advisory to help businesses adjust. And that is where the policy may fall flat.

“This isn’t just about amending tax laws,” says Dr Saima Khalid, a leading economist. “It’s about building the trust and infrastructure needed to wean a cash economy off its crutches.”

For now, businesses are left walking a tightrope, where paying by cash may not be illegal—but increasingly, it comes at a price.