Key Points

- Bloomberg Ranks Pakistan as Most Improved Emerging Market in Credit Risk Outlook

- The turnaround follows key milestones, including a $3 billion IMF deal

- Pakistan’s improved standing marks a rare bright spot in a region

ISLAMABAD: Pakistan has surged ahead as the standout emerging market in sovereign credit risk, posting the sharpest drop in default probability over the past year, according to a Bloomberg Intelligence analysis.

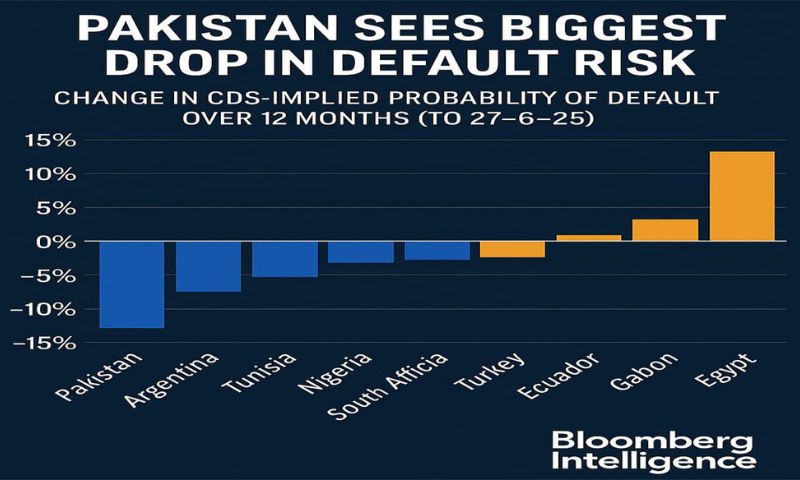

For a nation long shadowed by financial uncertainty, this development signals a major shift in how global investors perceive Pakistan’s economic resilience. Over the past 12 months, the country has recorded the sharpest decline in default probability among emerging markets—an 11 percentage point drop, from 59% to 47%—outpacing economic heavyweights like Argentina, Nigeria, and Tunisia.

Financial analysts often turn to Credit Default Swaps (CDS) as a pulse-check on sovereign credit risk. In this case, Pakistan’s falling CDS-implied default probability tells a hopeful story: the markets are starting to believe that the worst might be over.

Khurram Schehzad, Adviser to Pakistan’s Finance Minister, took to the social media platform X (formerly Twitter) on Saturday to share the development. “As per the latest data posted by Bloomberg Intelligence, Pakistan stands out globally as the most improved economy in terms of reduction in sovereign default risk,” he wrote.

Pakistan heading towards strong economic future: PM

Pakistan’s Prime Minister Shehbaz Sharif has also expressed satisfaction over the Bloomberg report.

In a statement, he said the report acknowledges important institutional reforms, successful agreements with the IMF, and timely debt repayments, which testify improvement in government’s economic performance. The Prime Minister said Pakistan is heading towards its strong economic future at a rapid pace.

From brink to bounce-back

The shift is as much psychological as it is statistical. In mid-2023, Pakistan’s economy teetered dangerously close to default, hampered by ballooning external debt, political uncertainty, and dwindling foreign reserves. Fast forward a year, and the narrative has changed.

The turnaround has been driven by a confluence of factors: macroeconomic stabilisation, a commitment to painful—but—necessary reforms, and a renewed partnership with the International Monetary Fund (IMF). Notably, Pakistan completed a $3 billion Stand-By Arrangement with the IMF earlier this year and is now seeking a longer-term Extended Fund Facility (EFF) to build on the progress.

Khurram Schehzad pointed to consistent debt servicing, a recovering rupee, narrowing current account deficits, and improving ratings outlooks from S&P and Fitch as key contributors to the shift in sentiment. “Pakistan is not only back on the map—it is moving forward with stability, credibility, and reform at its core,” he declared.

Regional standout

While Pakistan saw an 11 percentage point drop in default probability, other emerging markets showed less dramatic movements. Argentina improved by 7%, Tunisia by 4%, and Nigeria by 5%. By contrast, countries like Turkey, Egypt, Ecuador, and Gabon saw their CDS indicators worsen, suggesting an increased risk of default.

The news is particularly notable in a global economic climate where many developing nations are struggling with high interest rates, inflation, and weak capital inflows. Pakistan, once counted among the most at-risk economies, is now being cited as a case of surprising recovery.

Challenges remain

That said, the path ahead is far from easy. Inflation remains a pressing issue, and structural problems like energy inefficiency, tax shortfalls, and a narrow export base continue to constrain long-term growth. Public debt is still high, and meaningful economic reform must go beyond optics and into implementation.

Yet financial markets are forward-looking. The improved CDS readings reflect not just where Pakistan is today, but where investors believe it is headed. If confidence can hold, and reforms can deepen, the country might finally find itself on firmer fiscal footing.

Road forward

Pakistan’s economic managers know the journey is far from over, but recent data offers them something they haven’t had in a while: breathing room. The global spotlight has shifted—this time, not in warning, but in cautious optimism.

In a region where debt crises and currency devaluations are becoming alarmingly common, Pakistan’s improved credit standing isn’t just a footnote. It’s a headline. And for once, it’s the kind of headline that inspires hope.