This document is a snapshot of the changes brought into Finance Bill, 2023 vide Finance Act, 2023.

Income Tax

Virtual business presence in Pakistan included in definition of PE (New change). Defined as “including any business where transactions are conducted through internet or any other electronic medium, with or without having any physical presence.

SME definition was amended through FB 23 to increase annual turnover limit from PKR 250 million to PKR 800 million, and the FB 23 also included IT or IT enabled services in the definition of SMEs. The Finance Act 23 has omitted such change.

Section 7E exemptions ((a)one capital asset; (e) any property on which IT is chargeable under ordinance; (f) first year of acquisition subject to 236K payment; (g) where FMV excluding the exemptions does not exceed PKR 250 million) made inapplicable to persons not appearing in ATL other than persons not required to file return or statement under Rule 2 of Tenth Schedule. (New change)

Section 21(m), threshold increased to PKR 32,000/- from PKR 25,000/- (New change)

Section 37A Second proviso added, whereby Section 37A will not apply to disposal of shares; (A) Of a listed company made otherwise than through registered stock exchange and which are not settled through NCCPL; and (B) through IPO during listing process except where detail of the disposal is given to NCCPL for computation of capital gains and tax thereon under Section 37A.

(New change).

Section 44A (Exemption under Foreign investment (Promotion and Protection Act) 2022: The Finance Act has added advance tax under the purview of taxes to be exempted or subject to tax as provided under the captioned Act. It has also added that the said taxes will be subjected to tax as provided under the captioned Act. The Bill only provided for exemption.

Section 65I (Tax credit for construction of house): The said incentive introduced by FB 23 has been omitted in FA 23.

Section 99D (Tax on windfall income, profit, gains)

FB 23 had levied a tax on unexpected income, profit, gains. Whereas, FA 23 has levied a tax on windfall income, profit, gains.

FB 23 had levied this on every person. Whereas, FA 23 has restricted the scope of this tax to only companies.

FB 23 had levied the tax retrospectively as well for previous 5 tax years. FA 23 has decreased it to previous 3 tax years.

FA 23 has empowered Govt to determine through a Notification what windfall income, profit, gain will be. Said Notification shall be placed before the National Assembly within 90 days of passing thereof, or 30th June of the Financial Year, whichever is earlier.

Section 134A (ADR)

o Applies to;

▪ Tax liability of PKR 100 million or above; or

▪ Refund admissibility; or

▪ Waiver of default surcharge and penalty; or

▪ Any other specific relief required to resolve the dispute;

o Application for dispute resolution shall be made to the Board for appointment of a committee for the resolution mentioned in detail in the application.

o Dispute or hardship can be pending in any court of law;

o Cannot apply for ADR: where criminal proceedings have been initiated.

o Application for ADR shall be accompanied by: an initial proposition for resolution of the dispute, including an offer of tax payment.

o Board may appoint Committee within 15 days of receipt of such application

o Deemed stay till Committee Orders or dissolution of Committee, whichever is earlier.

o Order of committee binding on Commissioner where aggrieved person is satisfied with the decision and withdraws the appeal pending before any court of law or any appellate authority and has communicated the withdrawal order within 60 days of service of the decision of the Committee upon the aggrieved person.

o Aggrieved person shall make payment of income tax and other taxes within the time decided by the Committee.

o If Committee fails to decide within 60 days, the board shall desolve the Committee by a written order and the dispute shall be decided by the court of law or appellate authority.

Section 147 (Advance tax)

o Every person deriving income from business of

▪ construction and disposal of residential, commercial or other buildings; or

▪ development and sale of residential, commercial or other plots for itself or otherwise

o Liable to pay adjustable advance tax on a project by project basis as per tax rates in Part IIB of the First Schedule, in 4 equal instalments for the tax year. (New Change)

Section 236C (2A) introduced vide FA 23

o Any person responsible for registering, recording or attesting transfer of any immoveable property, shall not register, record or attest transfer, unless the sellor or transferor has discharged his / her Section 7E liability and provided evidence to this effect has been submitted to the said person in prescribed mode.

Section 236K – Exemption for Overseas Pakistani buyer or transferee from Advance tax The captioned exemption was introduced by FB 23. However, it has been removed vide FA 23.

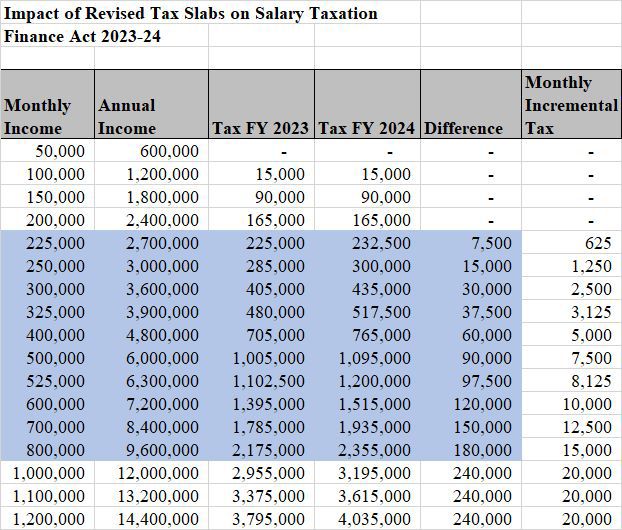

Tax rates for Individuals and AOPs increased (See Annexed Table)

Capital gain tax on securities acquired before July 01, 2013 has been zero rated

Advance tax on motor vehicles having engine capacity more than 2000cc has been based on value ranging from 6% to 10%.

For vehicles where engine capacity is not applicable (i.e. EV) and value os more than Rs. 5 m, the rate of advance tax will be 3%.

The rate of advance tax on sale/purchase of immovable property has been increased from 2% to 3%.

Sales Tax

Rate of further tax increased from 3% to 4%. (New change)

Limit of price for zero rating of preparations for infant milk for retail sale, increased from Rs. 500 to Rs. 600 per 200 gms. (New change)

DAP has been excluded from exempt fertilizers and has been subjected to 5% sales tax without input adjustment. (New change)

Exemption of following introduced in FB has been withdrawn:

a) Contraceptives and accessories thereof;

b) Bovine semen;

c) Saplings;

d) Combined Harvester-Thresher;

e) Dryer for agricultural products;

f) No-till-direct seeder, planters, trans-planters, and other planters;

g) Import of goods mention u/s 159 of Part III, Fifth Schedule of the Customs Act, 1969 (IV of 1969) chargeable to custom duty at 0% subject to restriction contained therein by the software exporters registered with Pakistan Software Export Board.

Wheat Bran, which is already exempted, has been provided back dated exemption since 01-07-2018.

Fixed tax of 1% and restriction of input tax adjustment has been extended to the supply chain in case of Drugs and Raw materials of APIs. Earlier, fixed tax regime was applicable only on

Importers and manufacturers.

Sales tax on Services (Islamabad)

Rate of tax IT and IT enabled services was changed from 16% to 5%(without input adjustment).

Now the rate has again increased to 15%.

FED

5% FED have been levied on fertilizers (New change)

Applicability of FED on levied on in efficient fans and Bulbs in FB has been effectuated from 01-01-2024.